Imagine you’ve been freelancing for a year. Business is good, clients are happy, and the money is coming in. Then out of nowhere, a client claims your work cost them money and threatens to sue. Without an LLC, that lawsuit doesn’t just threaten your business — it threatens your savings, your car, your home. So do you need one? That depends on a few things, and we’re going to walk you through all of them.

If you’ve been asking yourself “do I need an LLC for my business,” this guide covers what an LLC does, when it makes sense to form one, and when you might be fine without it. We’ll also explain how MyLLC can make the process simple from start to finish.

An LLC is not legally required, but it offers significant liability protection and tax flexibility for most business owners.

Without an LLC, you operate as a sole proprietor, meaning your personal assets are at risk if your business is sued or goes into debt.

An LLC can be taxed in multiple ways, giving you flexibility to optimize your tax situation as your business grows.

Forming an LLC through a professional service reduces the risk of costly paperwork mistakes.

An LLC, or Limited Liability Company, is a legal business structure that separates you from your business. If your business runs into financial trouble or gets sued, that separation generally keeps the problem from spilling over into your savings account, your home, or your personal property, provided you maintain the LLC as a distinct entity.

LLCs are popular because they’re flexible. You can run one as a single owner (a single-member LLC) or with multiple partners (a multi member LLC). You get liability protection without the formality of a corporation, and you can choose how the IRS treats your business for tax purposes, defaulting to pass-through taxation or electing corporate tax treatment.

Whether you need an LLC depends on your risk, your income, and where you want your business to go. Let's break it down by situation.

Short answer: probably yes, even if your side hustle feels small. If you sell products, offer services, or work with clients in any capacity, you have exposure. A customer slip at your pop-up, a product that causes harm, or a client dispute can hit your personal finances hard without an LLC in place. Forming one early costs relatively little and gives you protection as your income grows.

Freelancers often assume they don't need an LLC because they work alone. But if you have paying clients, sign contracts, or depend on your freelance income, an LLC is worth serious consideration. It separates your business obligations from your personal life, so creditors can't come after your personal bank accounts and property if something goes wrong. It also adds credibility when working with larger clients who prefer doing business with a formal entity.

If you're launching a business from the ground up, forming an LLC is one of the smartest early moves you can make. It establishes your business as a legal entity from day one, protects your personal assets before you've even landed your first client, and sets you up to open a business bank account, sign contracts, and build business credit. Starting with the right structure saves time and complications down the road.

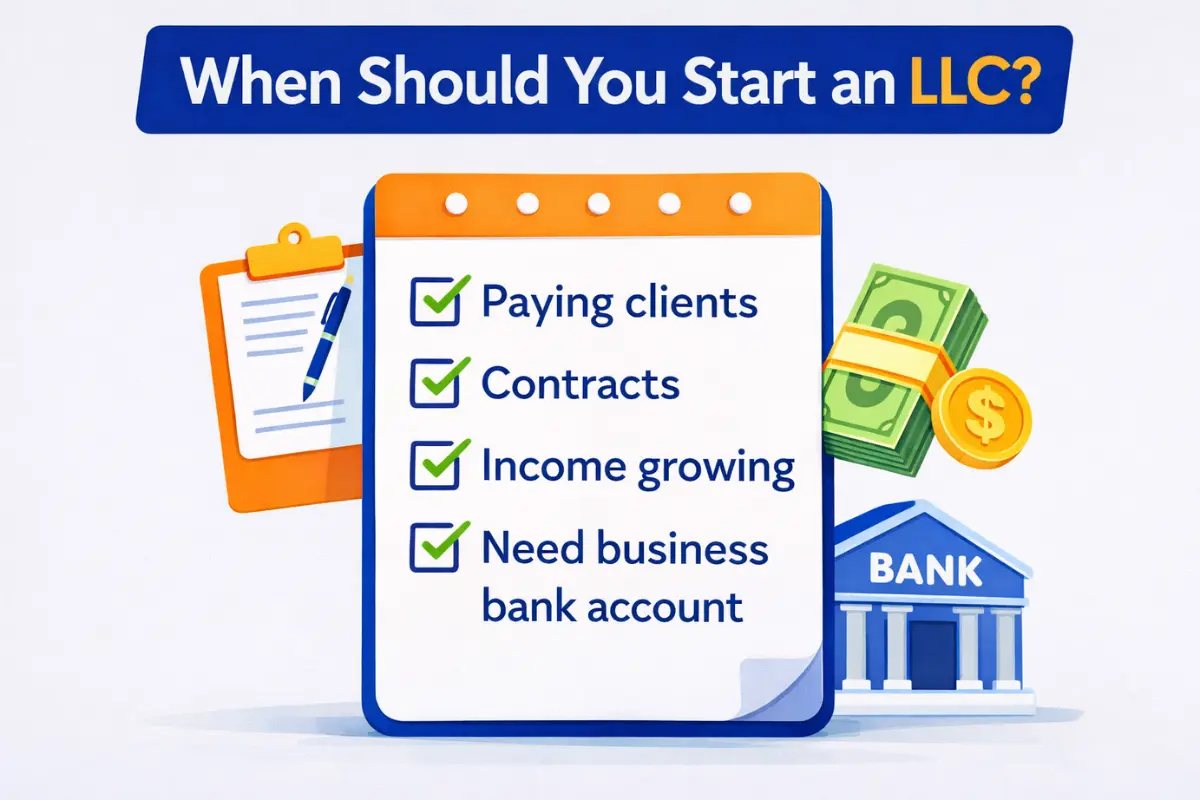

There’s no universal right time, but there are a few clear signals that it’s time to act:

You have paying clients or customers and are generating consistent income.

You’re entering into contracts with clients, vendors, or partners.

You want to open a dedicated business bank account or build business credit.

You want your business to look more professional and credible to clients.

If your business is generating meaningful income, carrying real risk, or you plan to sign contracts soon, form the LLC sooner rather than later, ideally before your first major client.

An LLC might not be the immediate priority if you’re truly just testing an idea with no clients, no contracts, and no real financial exposure. Operating as a sole proprietor temporarily is a reasonable choice. Some organizations, like nonprofits (which typically need a nonprofit corporation for 501(c)(3) status) or businesses pursuing major venture capital (which usually require a C-Corp), may need to think more carefully about the best business structure for their goals. But for the vast majority of small business owners, an LLC eventually makes sense. The question is usually not “if” but “when.”

There are several strong reasons why millions of business owners form LLCs each year:

Personal liability protection: According to the U.S. Small Business Administration, “LLCs protect you from personal liability in most instances,” meaning your personal assets are generally shielded from business debts and lawsuits, as long as you properly maintain the business structure.

Tax flexibility: An LLC can be taxed as a sole proprietorship, partnership, S-Corporation, or C-Corporation. This flexibility allows business owners to choose the most advantageous tax treatment as income grows.

Professional credibility: Having “LLC” after your business name signals to clients and partners that you’re a serious, established operation. It builds trust.

Easier banking and financing: Forming an LLC can make it easier to separate business and personal finances, open a dedicated business bank account, and build business credit.

Pass-through taxation: By default, LLC income passes through to your personal tax return, avoiding the double taxation associated with traditional C-Corporations.

Many business owners questioning whether they need an LLC are currently operating as sole proprietors by default. Here’s how the two compare:

| Factor | Sole Proprietorship | LLC |

|---|---|---|

| Liability | Unlimited personal liability | Limited personal liability |

| Taxes | Pass-through only (no options) | Default pass-through taxation, with option to elect S-Corp or C-Corp taxation |

| Setup | No registration required | Must file formation documents with the state and pay filing fees (typically $35–$500+, depending on state) |

| Credibility | Operates under personal name | Formal business identity with “LLC” or "Limited Liability Company" designation |

| Compliance | Minimal ongoing requirements | Ongoing requirements may include annual reports, registered agent, and state fees |

An EIN, or Employer Identification Number, is essentially a Social Security number for your business, used by the IRS to identify your company for tax purposes.

According to the Internal Revenue Service (IRS), you generally need an EIN to operate a limited liability company (LLC), especially if it has employees or files certain business tax returns.

The IRS also explains that “an LLC will need an EIN if it has any employees,” reinforcing that requirements depend on how your business operates.

Here’s when an LLC needs an EIN:

The LLC has employees.

The LLC is taxed as a corporation (S-Corp or C-Corp election).

The LLC is a multi-member LLC (more than one owner).

You want to open a business bank account (most banks require an EIN).

A single‑member LLC with no employees and no special tax filings may technically be able to use the owner’s Social Security number instead of an EIN. Still, getting an EIN is usually a smart move because it keeps your business and personal finances cleanly separated and protects your SSN from unnecessary exposure.

Here’s a step-by-step look at what’s involved. For a detailed, step-by-step walkthrough, visit our complete LLC formation guide.

Most business owners form their LLC in the state where they operate. Some states have lower fees or fewer reporting requirements, but your home state is usually the right starting point and helps you avoid extra registrations.

Your name needs to be unique in your state and must include “LLC” or “Limited Liability Company” (or an allowed abbreviation) in the title. States also require that your name be distinguishable from other businesses already on file.

Every LLC is required to have a registered agent. Not sure what that means? Learn more about what is a registered agent for LLC; it’s a person or service with a physical address in your state who receives official legal and state documents on behalf of the business.

This is the official document that registers your LLC with the state. It typically includes your LLC name, business address, registered agent information, and may include member or manager details, depending on your state’s requirements.

While not always required by law, this document outlines how your LLC is managed and how decisions are made. It’s especially important for multi-member LLCs, but even single-member LLCs benefit from having one to clarify ownership and procedures.

Obtaining your EIN correctly is an important step in most cases. Learn more about how to get an EIN for an LLC, or let MyLLC handle it accurately alongside the rest of your formation so nothing gets missed.

The cost of an LLC varies by state. Filing fees typically range from $35 to $500. Some states also charge annual report fees or franchise taxes. Additional costs may include a registered agent service or operating agreement preparation, but most business owners find it money well spent against the liability protection gained.

You can technically file your LLC paperwork on your own, but filing errors, missed requirements, or mistakes in your Articles of Organization can cause your formation to be delayed or leave gaps in your legal protection. State forms are not always user-friendly, and fixing errors often costs more than preventing them. Using a professional service like MyLLC gives you confidence that the paperwork is done correctly. Our team handles the details, and we provide registered agent services and ongoing compliance support so your LLC stays in good standing year after year.

No. An LLC is not legally required to run a business. But for most business owners, it’s a smart, affordable way to protect yourself and build long-term success. If you have customers, contracts, or income, the real question isn’t whether you need an LLC, it’s whether you can afford not to have one. For the vast majority of entrepreneurs and small business owners, an LLC hits the sweet spot: meaningful protection, tax flexibility, and manageable compliance requirements.

Yes. Learn more about single-member LLCs and how they work. This structure offers liability protection while keeping taxes simple as a pass-through entity.

An LLC provides strong liability protection, but it's not absolute. Courts can pierce the veil if you mix personal and business finances or ignore basic LLC formalities, so separate accounts and compliance matters.

Processing times vary by state. Some approve filings in a few days; others take several weeks. Expedited options are often available for an additional fee.

No. You can file an LLC yourself, but mistakes can delay approval or create gaps in protection. A formation service handles the paperwork accurately for far less than a lawyer.

Without an LLC, you're automatically a sole proprietor. Your personal assets, including your savings, home, and car, are fully exposed to business lawsuits and debts, because there's no legal separation.

Yes. By default, a single‑member LLC is taxed like a sole proprietorship, but you can elect S‑Corp treatment. With an S‑Corp, owners take a reasonable salary (subject to payroll taxes) and may take remaining profits as distributions that are not subject to self‑employment tax, which can save thousands. An LLC also makes it easier to separate business and personal finances for cleaner records at tax time.

Yes. An LLC can have one member or multiple owners, called LLC members. Multi-member LLCs are popular with partners because they combine limited liability with flexible profit sharing. When you have multiple owners, it's worth asking Do I Need an Operating Agreement for My LLC; it sets out ownership, decision-making, and what happens if a member leaves, so partner disputes are less likely to spiral.

Yes, and this is not optional if you want your LLC's liability protection to hold up. Mixing personal and business finances is one of the most common mistakes LLC owners make, and it can give courts reason to disregard your LLC status, leaving you personally responsible for business debts. A dedicated business bank account keeps your business assets separated from personal accounts, simplifies tax time, and helps you build business credit. Most banks require an EIN to open one.

Yes. An LLC can open a business bank account and build its own credit profile, which makes loans and vendor accounts easier to obtain. Lenders and many investors are more comfortable working with an LLC than with a sole proprietor, so having the right structure in place early can make fundraising smoother.

Forming an LLC doesn’t have to be complicated. Whether you’re just getting started or protecting a business you’ve already been running, we make the process simple.

Contact us today to get your LLC formed quickly and correctly, so you can move forward with confidence. MyLLC also offers registered agent services, EIN filing, and ongoing compliance support to keep your business in good standing every step of the way.