Consider this scenario: An entrepreneur has established a thriving enterprise generating $200,000 in annual revenue. A single lawsuit subsequently places their residential property at significant risk. The underlying cause? An inappropriate business structure selection.

This represents a genuine concern affecting business owners regularly. The organizational business structure you select determines your degree of personal liability for business obligations, your tax burden, and the extent to which your personal assets receive protection. An incorrect decision can result in substantial unnecessary tax expenditures while exposing your assets to considerable risk.

Understanding which business structure aligns with your business idea establishes the foundation for your entire business operation and long-term viability.

The selection of an appropriate business structure influences all aspects of operations, from daily management to long-term wealth accumulation:

Business structure affects taxes, legal liabilities, and compliance requirements. Your selection dictates how much you pay taxes, your personal responsibility for business debts, and regulatory obligations.

Strategic planning should inform structural decisions. Consider your business objectives for the next three to five years. A structure suitable for a $50,000 supplementary venture may prove inadequate for a $500,000 scaling operation.

Liability protection constitutes a critical consideration. Certain structures expose personal assets to business-related risks. Others establish legal barriers protecting your family's financial security and significant personal assets.

Tax implications have compounding effects. Thousands of dollars annually either remain available for business investment or are directed to tax payments, including self employment taxes and federal income taxes.

Professional consultation provides substantial value. Consulting a tax professional is minimal compared to the consequences of an inappropriate structural selection.

The business entity you select depends on key factors such as liability, tax treatment, and administrative or record‑keeping requirements. As the U.S. Small Business Administration explains, "The business structure you choose influences everything from day-to-day operations, to taxes and how much of your personal assets are at risk".

This decision influences whether business income is reported on your personal tax return or through a separate business return, the extent of your personal responsibility for business debts and obligations, and how easily you may attract investment or grow. The most suitable business structure aligns with your projected growth, risk profile, and compliance capacity while helping protect both personal and business assets.

Some business structures expose owners to unlimited personal liability for business obligations. Others provide significant personal liability protection, subject to proper formation and maintenance requirements. Choosing an appropriate structure can have a meaningful impact on your overall federal income tax and self‑employment tax burden, though the exact savings depend on your situation and applicable law.

Understanding the full spectrum of available business structures, including other business structures beyond the most common options, enables informed decision-making. Each business entity type offers distinct tradeoffs in liability protection, taxation, governance, and administrative complexity.

| Structure Type | Personal Risk | Tax Treatment | Complexity | Best For |

|---|---|---|---|---|

| Sole Proprietorship | Complete exposure | Personal taxes | Minimal | Concept validation |

| Partnership | Shared risk | Personal taxes | Low-moderate | Multi-owner ventures |

| LLC | Protected | Flexible | Moderate | Growing enterprises |

| S-Corporation | Protected | Personal taxes | Higher | Profitable LLCs |

| C-Corporation | Protected | Double taxation | Highest | Investment-seeking businesses |

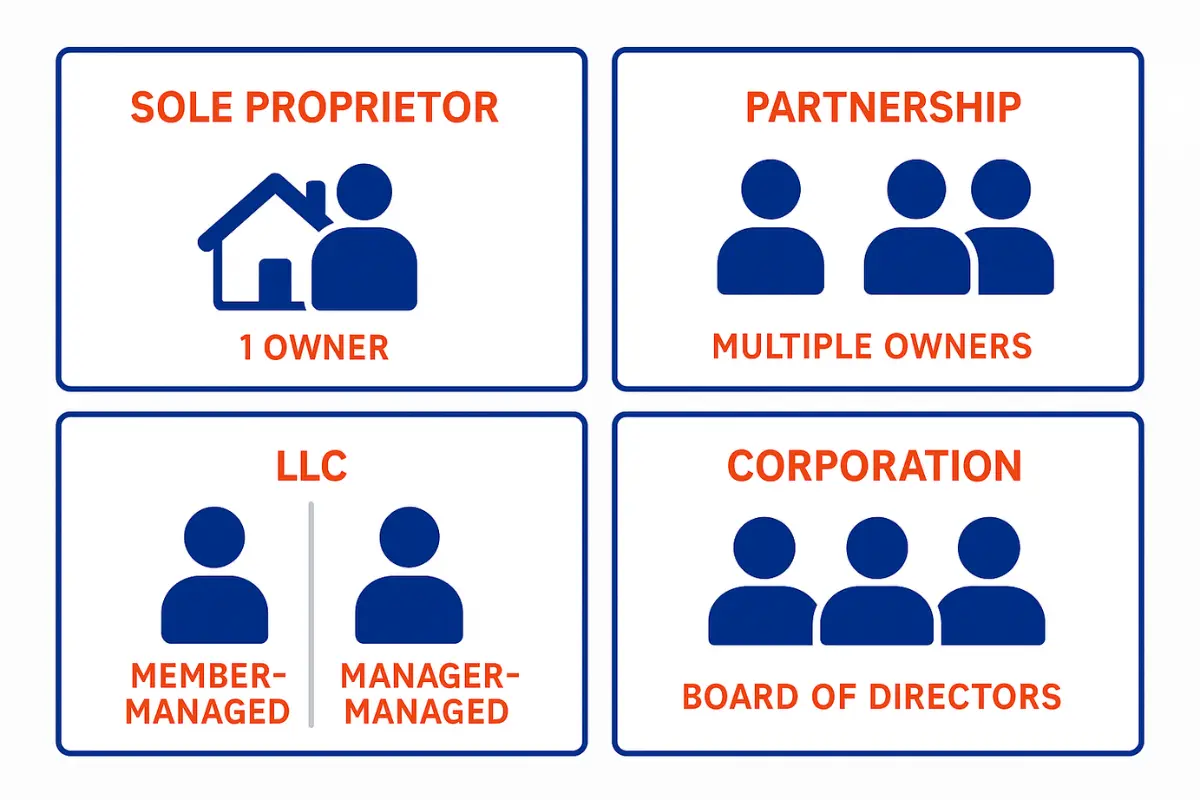

When an individual commences business activities and generates business income without formal registration, they establish a sole proprietorship by default. This unincorporated business owned by a single person represents the simplest legal entity structure, though the sole proprietor and the business entity are legally indistinguishable.

Business obligations become personal obligations. Legal actions target personal assets directly. As a sole proprietor, the owner is held personally liable for all business matters, creating unlimited liability exposure.

Example: An individual initiated a construction enterprise as an unincorporated business without formal registration. Following a structural failure, the resulting litigation placed their family residence and personal income at risk because they were personally liable for all business debts.

This structure may be appropriate for low-risk concept validation, but serious entrepreneurs and small business owners typically require more robust legal protection through a more formal business structure.

A general partnership forms automatically when multiple owners conduct business collaboratively without formal incorporation. This legal entity requires no formal business registration, making it another unincorporated business structure. General partners bear personal liability for all business decisions and operations, maintaining unlimited personal responsibility for partnership debts and the partnership's business assets.

Limited partnerships function differently within the general or limited partnership framework. Limited partners provide capital investment while receiving limited liability protection as passive investors, though general partners retain unlimited liability for business obligations. Both general partners and limited partners typically report income on their partners personal tax returns.

Both structures offer pass through taxation benefits. A formal partnership agreement can delineate roles and responsibilities, though it cannot eliminate personal liability for general partners who remain personally liable for all business debts.

Example: When foodborne illness affected a catering business operated as a general partnership, both partners' personal assets and partners personal assets faced potential legal exposure because they were held personally liable.

Many business owners elect to form a limited liability company (LLC) to circumvent these liability concerns and achieve better personal liability protection.

A limited liability company (LLC) establishes legal separation between personal and business assets, protecting personal assets including owners' residences, savings, and other personal property from business debts and legal claims. This limited liability company structure creates a formal business entity recognized under state laws. In most circumstances, if the LLC faces litigation, only the company's business assets are subject to risk, not the owners' personal assets.

However, limited liability protection is not absolute. Courts may "pierce the corporate veil" and hold members personally liable if they fail to maintain proper separation between business and personal finances, engage in fraudulent activities, or neglect to maintain the LLC as a distinct legal entity.

A limited liability company LLC provides substantial flexibility in tax treatment. By default, a single-member LLC is taxed as a sole proprietorship and reports business income on the owner's personal tax return, while a multi-member LLC with multiple owners is treated as a partnership. Owners may elect S Corp status or C Corp tax treatment by filing the appropriate Internal Revenue Service documentation. This flexibility enables business owners to optimize their tax strategy, including the ability to pay self employment taxes more efficiently through S Corp status.

To preserve legal separation and maintain limited liability, maintaining a dedicated bank account and accurate financial records is essential. Failure to maintain these standards can compromise liability protection and expose business owners to personal risk.

When a tenant initiated legal action against a rental property LLC, the owner's personal savings and residence remained protected due to proper LLC maintenance and consistent separation of business and personal finances, demonstrating the practical value of this structure for protecting personal assets.

For most small to medium-sized enterprises, a limited liability company provides an optimal combination of asset protection, favorable tax treatment, and operational simplicity.

C-Corporations (C-Corps) provide comprehensive liability protection and are particularly suitable for enterprises seeking venture capital investment or planning substantial expansion. The C Corp structure enables businesses to raise money through stock issuance and attract venture capitalists. However, a C Corp faces "double taxation": profits are subject to corporate taxes at the corporate level, and dividends are taxed again on shareholders' personal returns. C-Corps must comply with formal requirements as state laws typically govern corporations.

S-Corporations (S-Corps) do not constitute separate business entities but rather represent a tax election available to qualifying LLCs and corporations under Internal Revenue Code provisions. They enable pass through taxation, whereby profits and losses flow directly to owners personal income returns—thereby avoiding double taxation. Only U.S. citizens and residents may hold S Corp shares, with ownership limited to 100 shareholders. This S Corp structure provides significant advantages for certain business structures.

A significant advantage involves potential self employment taxes savings. In an S Corp, owners pay self employment taxes exclusively on their reasonable salary, while profit distributions are not subject to self employment taxes. Business owners can elect S Corp status to reduce how much they pay taxes annually.

Example: A consulting LLC generating $180,000 annually that elected S Corp status reduced self employment tax liability by approximately $11,000 per year—demonstrating how the right business structure affects overall tax burden.

| Element | C-Corporation | S-Corporation |

|---|---|---|

| Taxation | Double taxation | Pass-through |

| Ownership | Unlimited | 100 maximum |

| Requirements | Anyone | U.S. citizens/residents |

| Best For | Investment pursuit | Small business owners |

Every business must obtain appropriate licenses to conduct business legally and meet all legal obligations. Sole proprietors and partnerships need local business permits, sales tax registrations, and industry-specific professional certifications.

LLCs and corporations are established through state registration, creating a separate legal entity that provides limited personal liability protection. Regulated industries represent higher risk businesses requiring additional permits and certifications. Most financial institutions require registration documentation and an Employer Identification Number (EIN) from the Internal Revenue Service to establish a bank account for business purposes.

Each business entity has specific provisions governing taxation, liability, ownership, and profit distribution. Selecting the appropriate business structure can reduce risk and operational costs. Evaluate how each option affects asset protection, tax treatment, management structure, and funding flexibility.

Sole proprietorships and general partnerships do not provide limited liability protection for the owner or general partners, so their personal assets can be exposed to business-related debts and claims. By contrast, properly formed and maintained LLCs, corporations, and many LLPs generally separate business and personal assets, limiting owners’ or partners’ personal liability for most business obligations, subject to state law and exceptions such as personal guarantees or wrongful acts.

Pass through entities (sole proprietorships, partnerships, most LLCs, and S-Corporations) report business income on owners' personal tax returns, avoiding double taxation while requiring owners to pay self employment taxes. These pass through entities allow business income to flow directly to owners personal income without corporate-level taxation.

C-Corporations are subject to corporate taxes at both the corporate and shareholder levels. S-Corporations can reduce self employment taxes obligations by allocating income tax between salary and distributions. Benefit corporations operate as mission-driven for-profit entities without tax exempt status.

The IRS notes that your choice of business structure affects which income tax return you must file and that both legal and tax considerations are important when selecting a structure.

Sole proprietors maintain complete control over all business decisions within their management structure. Partnerships distribute management responsibilities according to partnership agreements. LLCs may be managed by members or designated managers, offering flexibility in their management structure. Corporations utilize boards of directors and corporate officers to oversee operations as state laws typically govern corporations.

Sole proprietorships require minimal formation costs but provide no liability protection. LLCs and corporations require state filing fees—typically ranging from $50 to $800—and may be subject to annual report fees or franchise taxes. Corporations generally incur higher compliance costs but offer superior growth advantages for raising capital.

Sole proprietors rely on personal funds. Partnerships pool capital from multiple owners. LLCs can attract investors and raise money through various mechanisms. C-Corporations raise capital most efficiently through stock issuance and venture capital attraction.

Sole proprietorships typically dissolve upon the owner's retirement or death. Partnerships require formal agreements for succession planning. LLCs and corporations continue operations beyond ownership changes, facilitating smoother transitions and supporting long-term organizational stability.

Your business structure determines operational management, control distribution, and liability exposure in daily operations.

Sole proprietorships and general partnerships are relatively simple to operate, but they do not create a legal separation between the business and its owners. Owners (and general partners) generally share management authority and also face unlimited personal liability for the business’s debts and obligations

Limited liability companies (LLCs) combine operational flexibility with liability protection. Members may manage the business directly or appoint managers, while personal assets generally receive protection from business liabilities, creating effective limited liability.

Corporations require formal governance structures with boards of directors and corporate officers. This framework supports growth, transparency, and continuity but demands stricter recordkeeping and regulatory compliance as state laws typically govern corporations.

Funding options vary by structure. Corporations may issue stock to raise money and attract venture capital, LLCs can add new members or investors, and pass through entities such as sole proprietorships and partnerships typically rely on personal funds or conventional loans.

Many entrepreneurs initially operate as a sole proprietor to validate their business idea with minimal expense, but this unincorporated business approach carries inherent personal liability risks. A limited liability company often represents a superior choice for businesses with financial exposure, providing immediate asset protection through formal business registration and creating a formal business structure.

As revenue increases or business assets accumulate, establishing an LLC or electing S Corp status can provide tax benefits and liability advantages. S corporation classification enables qualified businesses to reduce self employment taxes by compensating owners with a reasonable salary while treating remaining profits as shareholder distributions, allowing them to pay taxes more efficiently.

C-Corporations represent the preferred business structure for venture capital and public investment because they can issue multiple stock classes and accommodate unlimited shareholders. The C Corp structure facilitates raising capital from venture capitalists. LLCs with S Corp status often prove suitable for small to medium-sized enterprises until substantial external investment is pursued.

Selecting a business structure based exclusively on current requirements can necessitate costly transitions later. Consider your three-to-five-year growth projections, including potential additions of multiple owners, personal asset protection requirements, and tax implications including self employment taxes.

Sole proprietors bear personal responsibility for all business debts and litigation and remain personally liable for all business obligations. LLC or corporation owners receive limited liability protection, and S Corp status may significantly reduce self employment taxes obligations when business income exceeds modest levels.

Example: A business generating $120,000 could potentially achieve approximately $9,000 in annual tax savings under proper S corporation tax planning by reducing how much they pay taxes through strategic income allocation, though results vary.

While online resources provide general information, they cannot substitute for professional guidance from a tax professional or attorney. Tax professionals and attorneys ensure correct entity formation, regulatory compliance, and tax efficiency, potentially preserving thousands of dollars by avoiding misclassification or overlooking required filings.

The appropriate business structure affects all aspects of your operations, from daily decision-making and protecting personal assets to tax obligations and long-term ownership transitions.

Your selection influences how you pay taxes, liability exposure, and growth potential. Begin by evaluating each business entity type (sole proprietorship, partnership, limited liability company (LLC), or corporation) against your objectives and expansion plans.

Step 1: Assess. Determine your liability tolerance and evaluate whether you will operate in multiple states. Consider whether you need limited liability protection or can accept being personally liable.

Step 2: Prepare. Select a business name, define ownership percentages for multiple owners, and designate a registered agent. Maintain financial separation with a dedicated bank account for all business income and expenses.

Step 3: Consult experts. A tax professional and attorneys can clarify tax treatment, personal risk exposure, whether you'll pay self employment taxes, and compliance requirements for your chosen business structure.

Step 4: File and register. Submit state formation documents, apply for an Employer Identification Number (EIN) from the Internal Revenue Service, and secure all necessary licenses including sales tax permits.

The appropriate business structure protects personal assets, minimizes tax obligations, and positions your business for sustained growth.

Yes. Many entrepreneurs initially operate as a sole proprietor, then form a limited liability company for personal liability protection, then elect S Corp status for tax benefits or convert to a C Corp to attract venture capital. Advance planning is advisable because structural changes involve filings, fees, and potential tax implications affecting how you pay taxes.

Yes. Technology startups typically favor C-Corporations for venture capital funding. Law and accounting firms often utilize limited liability partnerships (LLPs). Freelancers and real estate investors generally prefer LLCs for risk management. Higher risk businesses particularly benefit from limited liability protection.

Yes. Incorporating “LLC” or “Inc.” in your business name enhances credibility and signals a formal business operation. C corporations convey scale and institutional legitimacy, while benefit corporations (B Corps) reflect social or environmental missions, though benefit corporations remain subject to taxation like standard corporations unless formally recognized as nonprofit organizations with tax-exempt status.

Without formal registration, you operate by default as a sole proprietor in an unincorporated business. You report business income on Schedule C of your personal tax return and maintain complete control, but you bear personal liability for all business debts and remain personally liable. Once significant business income or business assets are involved, forming a limited liability company or corporation represents the most prudent course for protecting personal assets.

An inappropriate selection can increase how much you pay taxes or elevate personal risk exposure. For example, remaining a sole proprietor could result in higher self employment taxes payments, while electing S Corp status prematurely may not justify the additional filing expenses. Structural adjustments are possible but require time and financial investment.

The business structure decision carries substantial implications that warrant professional guidance from a tax professional and legal experts. We manage legal requirements and documentation, enabling you to concentrate on business development while protecting personal assets.

Our comprehensive service offerings include business formation for all business entity types, registered agent services, and compliance assistance to maintain your business in good standing with all regulatory authorities and financial institutions.

Do not allow structural uncertainty to delay your entrepreneurial progress. Contact us today for expert guidance tailored to your specific circumstances and begin protecting your assets while optimizing how you pay taxes through the right business structure selection.