One lawsuit. One unpaid invoice. One unhappy client. Any of these could wipe out everything you’ve worked for if your business isn’t properly structured. That’s the reality most entrepreneurs don’t think about until it’s too late.

Forming an LLC puts a legal wall between your personal assets and your business. It protects your savings, adds credibility, and gives you real tax flexibility. But it isn’t the right fit for every situation, and we want to give you an honest look at whether it makes sense for yours.

Our team at MyLLC has helped thousands of entrepreneurs work through this decision. Here’s everything you need to know about the pros, cons, costs, and benefits before you decide.

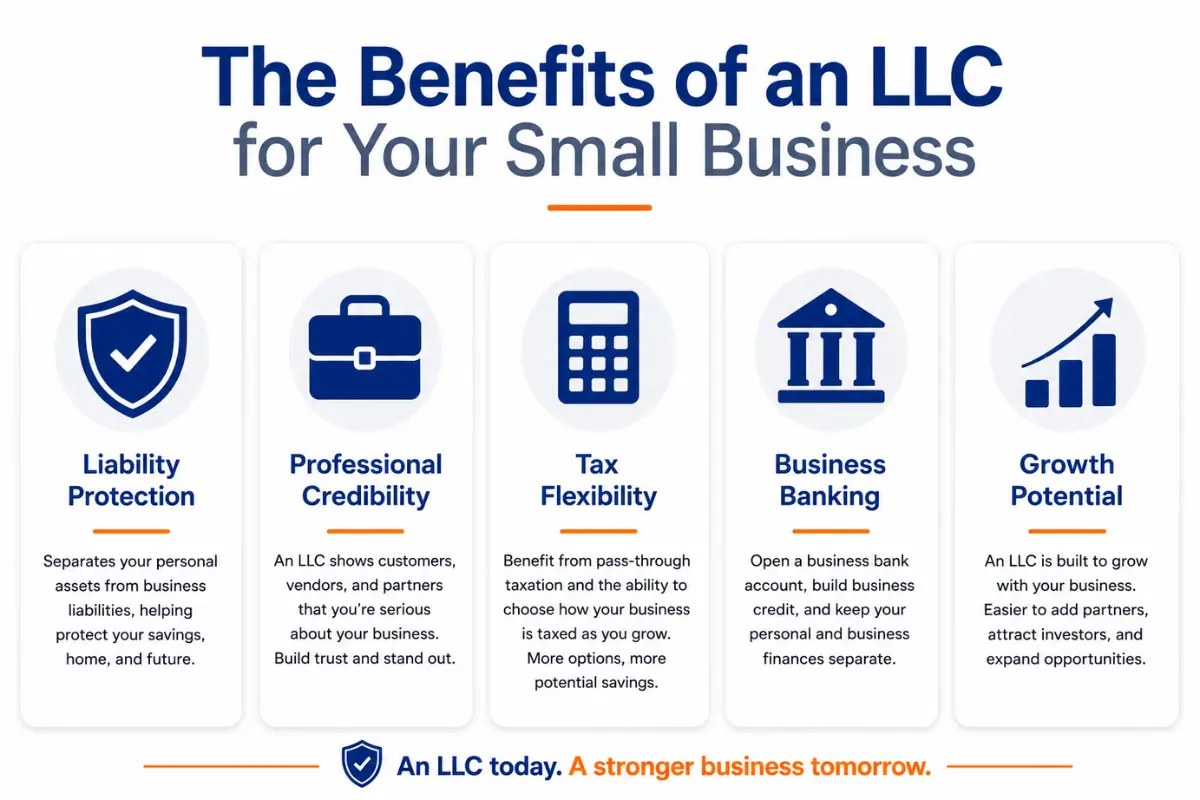

An LLC protects personal assets from many business liabilities.

LLCs improve credibility with customers, banks, and vendors.

Most LLCs benefit from pass-through taxation.

LLCs require state filings, fees, and ongoing compliance.

For many small businesses, the protection and flexibility outweigh the costs.

Before deciding whether forming an LLC is worth it, it helps to understand what an LLC actually is and how to start an LLC.

A limited liability company (LLC) is a business structure that creates a separate legal entity for your business. That separation is the whole point. It means your personal assets, your home, your savings, your personal bank account, are generally shielded if your business faces a lawsuit or can’t pay its debts.

An LLC blends the liability protection of a corporation with the tax benefits of a partnership. You get real legal protection without rigid corporate formalities like holding shareholder meetings or maintaining a board of directors.

A sole proprietorship has no legal distinction between you and your business. An LLC creates that wall. That difference matters enormously if something goes wrong.

Forming an LLC is worth it when any of these apply:

You have liability exposure. If a client could be injured or your work carries professional risk, you need personal liability protection.

You’re signing contracts. When you sign as a sole proprietor, you’re personally on the hook if something goes wrong. An LLC signs as its own entity.

You’re hiring employees. Employment brings legal obligations. An LLC helps contain that risk exposure.

You have growth plans. An LLC is easy to scale, add members to, and adapt as your business evolves.

You run an online or e-commerce business. Even digital businesses carry liability risk tied to products, services, or customer disputes.

You’re running a low-risk hobby business with minimal revenue.

You’re testing a temporary idea and haven’t committed to it yet.

Your business generates little income and carries virtually no liability risk.

That said, most business owners reach the right time for an LLC sooner than they expect. Once you start working with clients or earning consistent income, the protection becomes worth the cost quickly.

Many freelancers and solo entrepreneurs choose a single-member LLC to separate personal and business liabilities. It’s one of the most straightforward ways to protect yourself when running a business on your own.

Personal asset protection. Your personal finances stay separate from business liabilities. If your business is sued or owes a debt, your personal savings and property are generally protected.

Professional image. Having “LLC” after your business name signals to clients, lenders, and vendors that you’re running a legitimate, established business.

Easier business banking. Many banks require a formal business entity to open a business bank account, keeping your business funds and personal finances cleanly separated.

Separation of finances. Keeping personal and business finances apart protects your liability shield and makes tax time much simpler.

Consultants and coaches

Freelancers and creative professionals

Contractors and tradespeople

Real estate investors

Online sellers and e-commerce owners

An LLC offers more than just a formal business name. It provides real, tangible protections that can shield your personal finances, improve credibility, and create a stronger foundation for growth. For business owners with partners, a well-drafted LLC operating agreement is essential to defining how a multi-member LLC is managed and how important decisions are made. Here are some of the most significant benefits of choosing an LLC.

An LLC creates a legal barrier between your personal assets and your business liabilities. According to the U.S. Small Business Administration (SBA), owners of an LLC are generally not personally liable for the company’s debts and liabilities.

Without that protection, a single lawsuit or unpaid debt could put your home, savings, and personal finances directly at risk. An LLC keeps that exposure at the business level, where it belongs.

An LLC signals to the world that you’re serious. Customers trust formally registered businesses. Lenders are more willing to extend credit. Vendors engage more readily. For many small business owners, this credibility boost alone makes forming an LLC worth the cost.

LLCs offer flexible ownership and management structures. You can operate solo or bring in partners, manage day-to-day operations yourself, and avoid the corporate formalities that come with a C corp or S corp structure. There are no required shareholder meetings or board resolutions to worry about.

An LLC grows with you. You can add members, obtain financing more easily, and change your tax status as your income increases. That adaptability is hard to match with other business structures.

By default, an LLC does not pay federal income taxes as a separate entity. The IRS classifies LLCs as pass-through entities, meaning business profits and losses flow through to the owner’s personal tax return and are taxed once at the individual level.

According to the Internal Revenue Service (IRS), a single-member LLC is generally treated as a disregarded entity for federal income tax purposes, while a multi-member LLC is generally treated as a partnership unless it elects another tax classification.

This avoids the double taxation that C corporations face, where profits are taxed at the corporate level and again when distributed to shareholders.

One of the most powerful advantages of an LLC is tax flexibility. Once your business income reaches a certain level, you can elect S corp status to reduce self-employment taxes. You pay yourself a reasonable salary and take additional profits as distributions, which aren’t subject to self-employment taxes. Most LLC owners will also need an EIN to properly file taxes and set up business banking. The savings can be significant.

An LLC also makes it easier to properly document and deduct legitimate business expenses. Keeping business and personal finances separate makes it simpler to qualify expenses properly and lower your taxable income. LLC owners may also qualify for a special pass-through deduction under the Tax Cuts and Jobs Act, allowing eligible business owners to deduct up to 20% of net business income each year.

Common deductible expenses include:

Home office expenses

Equipment and software purchases

Business travel and vehicle expenses

Tax savings vary by business type and income level. For lower-income businesses, the tax advantages might be modest on their own. But when you combine them with liability protection and credibility, the full picture is compelling for most small business owners. A qualified tax professional can help you determine the most appropriate course of action for your specific income level.

Yes, and many people do. Real estate investors commonly form LLCs to hold rental properties, keeping each property in its own legal entity so a lawsuit related to one can’t touch assets in another.

According to the IRS, LLCs are permitted under state statute and can be used for a variety of business and investment activities depending on state law and ownership structure.

Asset separation. Keeping investment properties or high-value assets in an LLC separates them from your personal finances.

Privacy. Some states allow LLC ownership to limit public disclosure.

Risk management. If you own assets that could generate liability, like rental properties, an LLC helps contain that risk.

Personal-use LLCs still carry state filing fees, annual report fees, and registered agent costs. It’s worth weighing those ongoing expenses against the protection and tax advantages you gain.

State filing fees for establishing an LLC typically range from $50 to $200, though some states charge more. Additional costs can arise from licenses or permits depending on your industry. Most states also require annual reports and ongoing fees to keep your LLC in good standing, plus a registered agent, which adds another recurring cost. For business owners with low or seasonal income, these requirements can feel like an added burden, which is worth factoring into your decision.

An LLC comes with recordkeeping and compliance obligations. You’ll need to track business finances separately, file required state reports, and maintain your status. Letting compliance lapse can weaken your liability protection.

LLC owners pay self-employment taxes on their share of business profits, covering both the employer and employee portions of Social Security and Medicare. This adds up at higher income levels, which is why many profitable LLCs eventually elect S corp status.

Some states charge franchise taxes or additional fees on top of standard requirements. California, for example, charges a minimum franchise tax regardless of whether the LLC earns a profit. Know your state’s rules before you form.

Choosing between an LLC and a sole proprietorship comes down to how much risk you're willing to carry personally. And if you're weighing even more options, our breakdown of an LLC vs corporation can help you see the full picture.

The differences between these two structures come down to one core issue: legal separation. As the SBA explains, a sole proprietorship is the simplest business structure to establish, but it does not create a legal separation between the owner and the business. Here is how the two compare across the factors that matter most.

| Factor | LLC | Sole Proprietorship |

|---|---|---|

| Liability Protection | Yes – limited personal liability | No – owner personally liable |

| Formation Requirements | State filing and fees required | Very simple, often automatic |

| Credibility | Often viewed as more formal/credible | Often viewed as less formal |

| Tax Treatment | Default pass-through, options available | Pass-through to owner |

| Compliance Requirements | Annual filings and records common | Fewer formal requirements |

A sole proprietorship might work if you’re running a very low-risk business, testing an idea, or generating little income with no employees. The appeal is simplicity. But that simplicity comes at the cost of personal liability protection, which catches many sole proprietors off guard when something goes wrong.

An LLC is the better choice when you’re ready to protect personal assets, when revenue is growing, or when you’re taking on greater risk through contracts, employees, or client services.

Liability protection separating personal and business assets

Enhanced credibility with clients, lenders, and vendors

Tax flexibility including the option to elect S corp or C corp status

Easier business expansion, including adding members and securing financing

Formation costs including state filing fees and registered agent fees

Annual compliance obligations including reports and recordkeeping

LLCs cannot issue stock, which can limit access to venture capital for businesses planning significant outside investment

Simple setup with no formal registration required

Minimal startup costs

Less paperwork and fewer ongoing requirements

Unlimited personal liability, your personal assets are fully exposed

Fewer growth opportunities and limitations on attracting investors

Less credibility with clients, banks, and vendors

If your LLC isn’t generating revenue yet, you might worry you’re paying fees for nothing. Here’s what you need to know:

Most states still require annual reports and fees regardless of revenue.

You may still have tax filing requirements even if business income is zero.

Registered agent costs continue regardless of business activity.

Yes. Many business owners keep their LLC active during slow periods because maintaining good standing costs far less than dissolving and reforming later. It preserves your business name, your legal structure, and your options for future growth.

Forming an LLC is an investment, and like any investment, the returns depend on your situation. Understanding the cost of an LLC upfront helps you weigh whether the protection, credibility, and tax advantages justify what you'll spend to get started.

State formation fees (typically $50 to a few hundred dollars)

Annual report fees and state renewal costs

Registered agent service fees

Compliance and administrative costs

Asset protection that keeps your personal finances safe

Tax flexibility that can reduce your tax burden as income grows

Credibility that opens doors with clients, banks, and vendors

Growth potential with a structure that scales alongside your business

Ask yourself these questions before deciding:

Do I have personal assets I need to protect?

Am I working with clients or signing contracts?

Is my business generating consistent revenue?

Do I plan to grow, hire, or bring on partners?

Would a more professional image help me win more business?

If you answered yes to most of these, forming an LLC is very likely worth it for your situation.

For most entrepreneurs, yes. An LLC offers personal liability protection, tax flexibility, and business credibility that is hard to match at a comparable cost.

The value depends on your risk level, your revenue, and your long-term goals. But for anyone working with clients, signing contracts, or building a business with real growth potential, the protection alone justifies the cost.

Forming an LLC is an investment in protecting what you’ve built and giving your business the foundation it needs to grow with confidence.

Forming an LLC doesn’t have to be complicated. Our team at MyLLC handles the paperwork and filing requirements so you can have confidence it’s done right. Contact us today to get started.

It depends on your risk exposure. If you're working with clients or signing contracts, an LLC is worth considering even at lower income levels. The liability protection matters regardless of revenue. For a pure hobby with no clients and minimal risk, it may make sense to wait until your business grows.

Often, yes. Once your side hustle starts generating real income, working with clients, or taking on any risk, an LLC provides important protection. Many side hustlers wish they had formed one sooner after experiencing a dispute or unexpected tax situation.

For many business owners, yes. Pass-through taxation, the potential 20% pass-through deduction, and the option to elect S corp status make an LLC one of the most tax-efficient structures available. The benefits grow more significant as your business income increases.

Yes, you can transition at any time. The process involves filing Articles of Organization with your state and updating your business accounts and contracts. The sooner you make the switch, the sooner your personal assets are protected.

The main disadvantages of an LLC are the ongoing costs and administrative responsibilities, including state fees, registered agent costs, and compliance requirements. For very low-revenue businesses, these costs can feel disproportionate, though most business owners find them well worth it.

Yes, in most cases. Working from home doesn't eliminate liability risk. If clients visit your home office, you ship products, or you provide professional services, you can still face legal claims. An LLC protects your personal property from those business-related risks.