So you have got a business idea, maybe even a business already up and running. Then you hear the term “LLC” and start wondering: do you actually need one, or is operating as a sole proprietor good enough?

It is a question we hear all the time at MyLLC. When comparing LLC vs sole proprietorship, the real answer comes down to how much risk you are willing to take on and how you want your business to grow. Your business structure affects everything from your tax obligations to your personal liability and long-term flexibility.

Understanding the key differences between an LLC and a sole proprietorship could be one of the most important decisions you make for your business this year. This guide breaks down LLC vs sole proprietorship in simple terms, so you can choose the right structure with confidence and move forward without second-guessing.

An LLC protects your personal assets; a sole proprietorship does not

Both structures use pass-through taxation by default

Sole proprietorships are simpler and cheaper to start

LLCs offer more protection and long-term flexibility

The right choice depends on your risk level, income, and growth plans

A sole proprietorship is the simplest business structure out there. There is no formal registration, no separate legal entity, and no real barrier between you and your business.

As the IRS explains, a sole proprietor is someone who owns an unincorporated business by themselves. The business and the owner are treated as one and the same.

That simplicity is appealing, but the downside is significant. If your business gets sued or runs up debt, your personal bank account, car, and home are all fair game. Sole proprietorships work best for very small, low-risk operations where the owner is comfortable assuming full personal responsibility.

An LLC, or limited liability company, is a formal business structure that creates a legal separation between you and your business. That separation is the key difference.

When you form an LLC, you establish a distinct legal entity. The business can enter contracts, own property, and take on debt in its own name. If something goes wrong, creditors generally go after the business, not your personal savings.

LLCs also offer flexible tax treatment. You can choose how the IRS categorizes your LLC, which gives you options as your income grows. And unlike corporations, LLCs do not require board meetings, complex bylaws, or heavy compliance overhead.

Here is a quick side-by-side comparison of the most important factors:

| Factor | LLC | Sole Proprietorship |

|---|---|---|

| Liability | Limited — personal assets protected | Unlimited — full personal exposure |

| Taxes | Pass-through (flexible; S corp election available) | Pass-through (reported on personal return) |

| Cost | State filing fees ($50 to $500) | No formation cost |

| Compliance | Annual reports, registered agent required | Minimal |

| Credibility | Higher — "LLC" in name adds legitimacy | Lower — no formal structure signal |

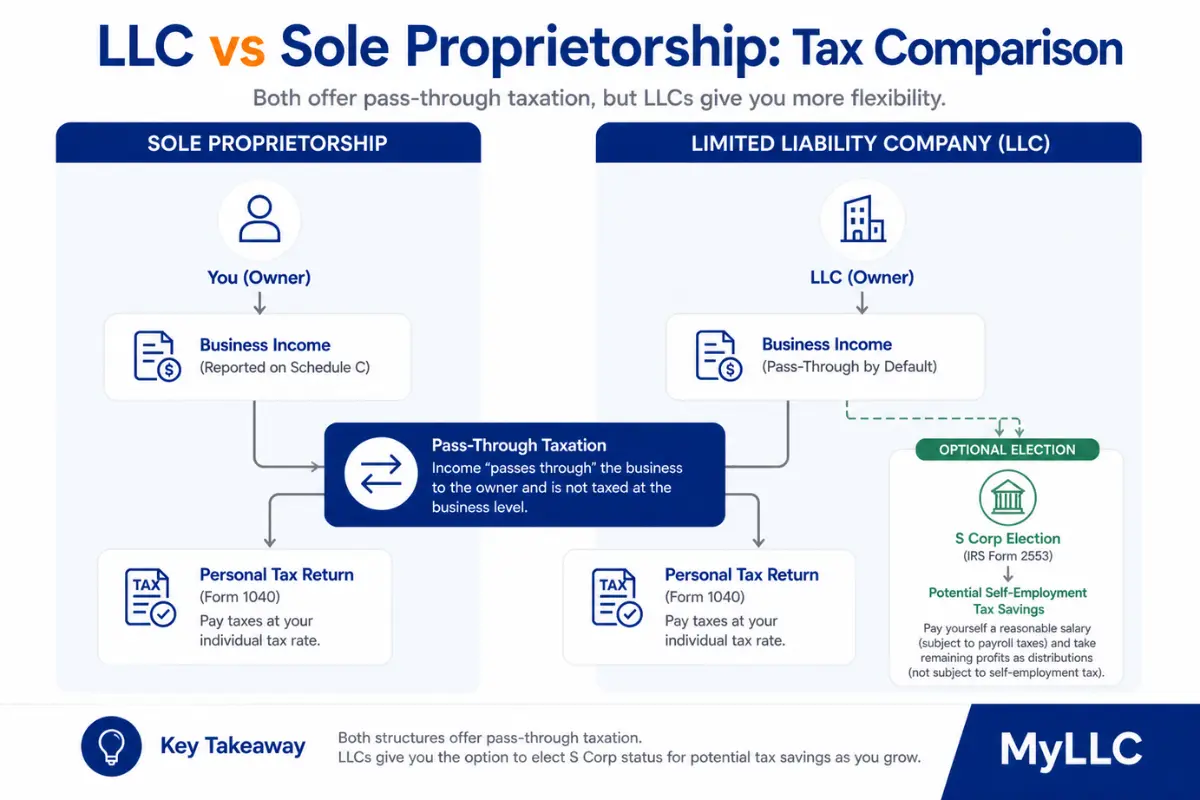

Here is some good news for both structures: by default, neither one pays taxes at the business level. Both use pass-through taxation, meaning profits flow through to your personal tax return.

The IRS explains that by default, single-member LLCs are treated as disregarded entities for federal tax purposes. In plain terms, the IRS largely ignores the LLC itself and taxes the owner directly, just like a sole proprietor.

Where things get interesting is with self-employment taxes. Both sole proprietors and LLC owners typically owe self-employment tax on their net earnings, which runs around 15.3 percent. However, LLC owners have an option that sole proprietors do not: they can elect to be taxed as an S corporation once their income reaches a level where that makes sense. That election can meaningfully reduce the self-employment tax burden by allowing owners to take some income as distributions rather than salary.

This article is for informational purposes only and not tax advice. Consult a qualified tax professional for guidance tailored to your circumstances.

A single member LLC is owned by one person, making it easy to compare directly to a sole proprietorship. On the surface, they look similar from a tax standpoint: both default to pass-through taxation on the owner's personal return.

The critical difference is legal protection. A sole proprietor and their business are legally the same. A single member LLC creates separation, shielding personal assets from business liabilities like lawsuits or debts (though protection isn't absolute if misconduct pierces the veil).

This is exactly why so many sole proprietors make the switch. The tax situation stays roughly the same, but they gain a layer of protection that was not there before.

Liability protection keeps personal assets separate from business risk

Adds credibility and professionalism to your business name

Flexible tax options, including S corp election for higher earners

Easier to bring in partners or investors as the business grows

State filing fees ranging from $50 to $500 depending on location

Ongoing compliance requirements like annual reports and a registered agent

Slightly more administrative work than operating as a sole proprietor

Extremely easy to start, no formal registration required

No formation costs and minimal ongoing paperwork

Simple tax filing, business income goes directly on your personal return

Unlimited personal liability for all business debts and lawsuits

Harder to scale, attract clients, or secure funding without a formal structure

No separation between personal and business finances

When you compare the two structures side by side, the LLC consistently comes out ahead for anyone building something with real stakes involved.

The biggest benefit is asset protection. As the U.S. Small Business Administration notes, forming an LLC can help protect your personal assets if your business is sued or incurs debt. That protection is not something a sole proprietorship can offer.

LLCs also carry more credibility. Having "LLC" in your business name signals to clients, vendors, and banks that you are operating a legitimate, formal business. That can make it easier to land bigger contracts, open business bank accounts, and establish credit.

And when it comes to growth, an LLC gives you options. You can bring in members, adjust your tax structure, or evolve into a corporation down the road. A sole proprietorship is a dead end from a structural standpoint.

There are a few situations where making the switch from sole proprietor to LLC becomes pretty urgent.

If your business risk is increasing, whether that means working with clients on physical job sites, handling sensitive data, or managing higher-value contracts, the exposure gets real fast. One lawsuit can wipe out savings you spent years building. An LLC creates a buffer.

Higher income levels are another trigger. Once your business is generating meaningful profit, the tax flexibility of an LLC starts to pay off. And if you are hiring employees or working with larger clients who require formal contracts, an LLC is often expected.

The U.S. Chamber of Commerce highlights that LLCs offer greater flexibility and protection than sole proprietorships, which is why many small business owners choose this structure. It is not a complicated decision once you understand what is at stake.

Sole proprietorships tend to work best for low-risk, early-stage ventures where someone is testing a concept before committing to a formal structure. Think of a freelance writer just picking up their first few clients, or someone selling handmade items at a local market.

But once any real money or risk enters the picture, an LLC makes more sense. A personal trainer building a client roster, a contractor taking on large projects, a consultant working with corporate clients, these are all situations where having an LLC is not just smart but arguably necessary.

Making the transition is more straightforward than most people expect. Here are the key steps:

Your LLC name needs to be unique in your state and include "LLC" or "Limited Liability Company." Check availability through your state's business registry before committing.

Every LLC is required to have a registered agent, which is a person or service designated to receive legal documents on behalf of the business. Many business owners use a professional service to handle this.

This is the formation document that officially creates your LLC. You file it with your state's business office and pay the associated fee. The specifics vary by state.

An operating agreement serves as your LLC's internal roadmap, detailing management structure, owner roles, profit sharing, and procedures for changes like member exits. Though rarely mandated by state law, it clarifies operations, overrides default rules, and bolsters liability protection, essential even for single-member LLCs.

An Employer Identification Number is like a Social Security number for your business. You will need it for business banking, hiring employees, and filing taxes. The IRS application is a straightforward process.

Once your LLC is officially formed, update any existing business licenses, open a dedicated business bank account under the LLC, and notify vendors and clients of the new entity name.

Not sure which way to go? Run through this quick checklist:

Risk level: Are you in an industry where lawsuits or liability are a realistic concern? If yes, an LLC is the safer choice.

Revenue: Are you generating consistent income? Higher earnings make LLC tax flexibility more valuable.

Growth plans: Do you plan to hire employees, bring in partners, or scale significantly? An LLC gives you the structure to do that.

Administrative comfort: Are you willing to handle some annual compliance tasks? If so, an LLC is manageable. If not, a professional service can help.

Choosing between a sole proprietorship and an LLC comes down to how much risk you are willing to carry and where you want your business to go.

Sole proprietorships are simple to start, but they leave you fully exposed. LLCs take a little more effort upfront but deliver real protection and room to grow. For most business owners, the choice is clear.

Forming an LLC does not have to be complicated. Our team at MyLLC handles everything for you, from filing your Articles of Organization to setting you up with registered agent services and ongoing compliance support.

Skip the paperwork, avoid the guesswork, and get your LLC formed the right way. Contact us today to get started.

There is no universal number, but many advisors suggest considering an LLC once you are consistently earning $30,000 or more from your business. The liability protection alone often justifies the cost before that, and the tax flexibility becomes more valuable as income grows.

Cost and compliance. You will pay state filing fees to form the LLC and often an annual fee to keep it active. You also need to maintain a registered agent and file annual reports in most states. These are manageable requirements, but they are real compared to the zero-overhead nature of a sole proprietorship.

Yes, and it is more common than you might think. Many business owners start as sole proprietors and later formalize into an LLC as their income and risk exposure grow. The process involves filing with your state, getting an EIN, and updating your banking and licenses.

In many cases, yes. While both structures use pass-through taxation by default, an LLC gives you the option to elect S corp status once your income reaches a level where that is beneficial. That election can reduce what you pay in self-employment taxes, which adds up to real savings over time.

An LLC separates you from the business, shielding personal assets (property, finances) from business liabilities while business assets stay with the entity. Protection isn't absolute—if you guarantee loans, mix finances, or neglect formalities, courts can pierce it. Maintain separate accounts and records to preserve the shield.

Both default to pass-through taxation on your personal return. LLCs offer flexibility like S-corp election to cut self-employment taxes on higher income; sole proprietors pay SE tax on all net earnings with no such option. Consult a tax professional for your situation.

Yes. Sole proprietorships limit to one owner with full control. Multi-member LLCs allow shared ownership, profits, and management via an operating agreement, which customizes rules or defaults to state law. This provides more structure and flexibility than sole proprietorships.

Generally, yes. Lenders and investors tend to view an LLC more favorably than an unregistered sole proprietorship because it signals business credibility and a formal business entity. Some lenders specifically require you to operate as an LLC or corporation before approving business loans. An LLC also makes it easier to separate business expenses from personal finances, which strengthens your financial records and makes applications cleaner. For low risk businesses just starting out, the added credibility of an LLC can open doors that a sole proprietorship cannot.